Category: Money Management Product Reviews

Money Management Product Reviews

Money Management Product Reviews

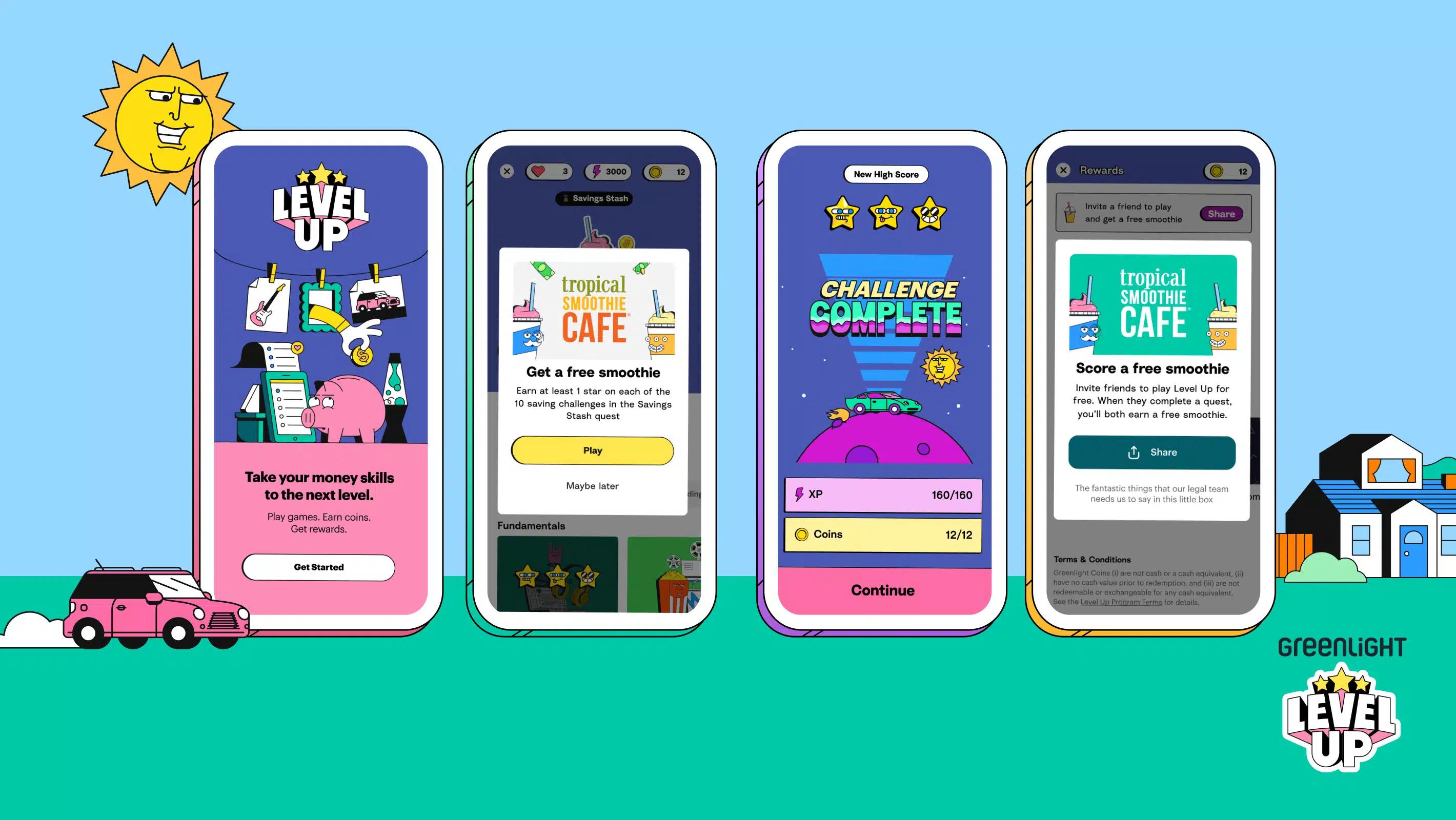

Greenlight Level Up Review: A Free Financial Literacy Game

Despite personal finance being an important topic for those of all ages, few schools make it a part of their curriculum. In this absesnse, several companies and institutions have offered their own ways for children, teens, and adults to gain financial literacy. Among those looking to lend some assistance is Greenlight, which now offers a free financial learning game called Level Up. Even better, the company recently announced a partnership...

Money Management Product Reviews

Pepper Rewards Review: Earn Rebates on Gift Cards from Top Brands

Recently, out of nowhere, an app called Pepper seemed to be all the rage in the credit card reward and deal-finding corner of the Internet. Unlike some other apps I've seen mentioned that just seem too convoluted to be worth it, the premise of Pepper is super simple: buy gift cards and earn rewards. While there are some other sites where you can buy discounted gift cards or other apps...

Money Management Product Reviews

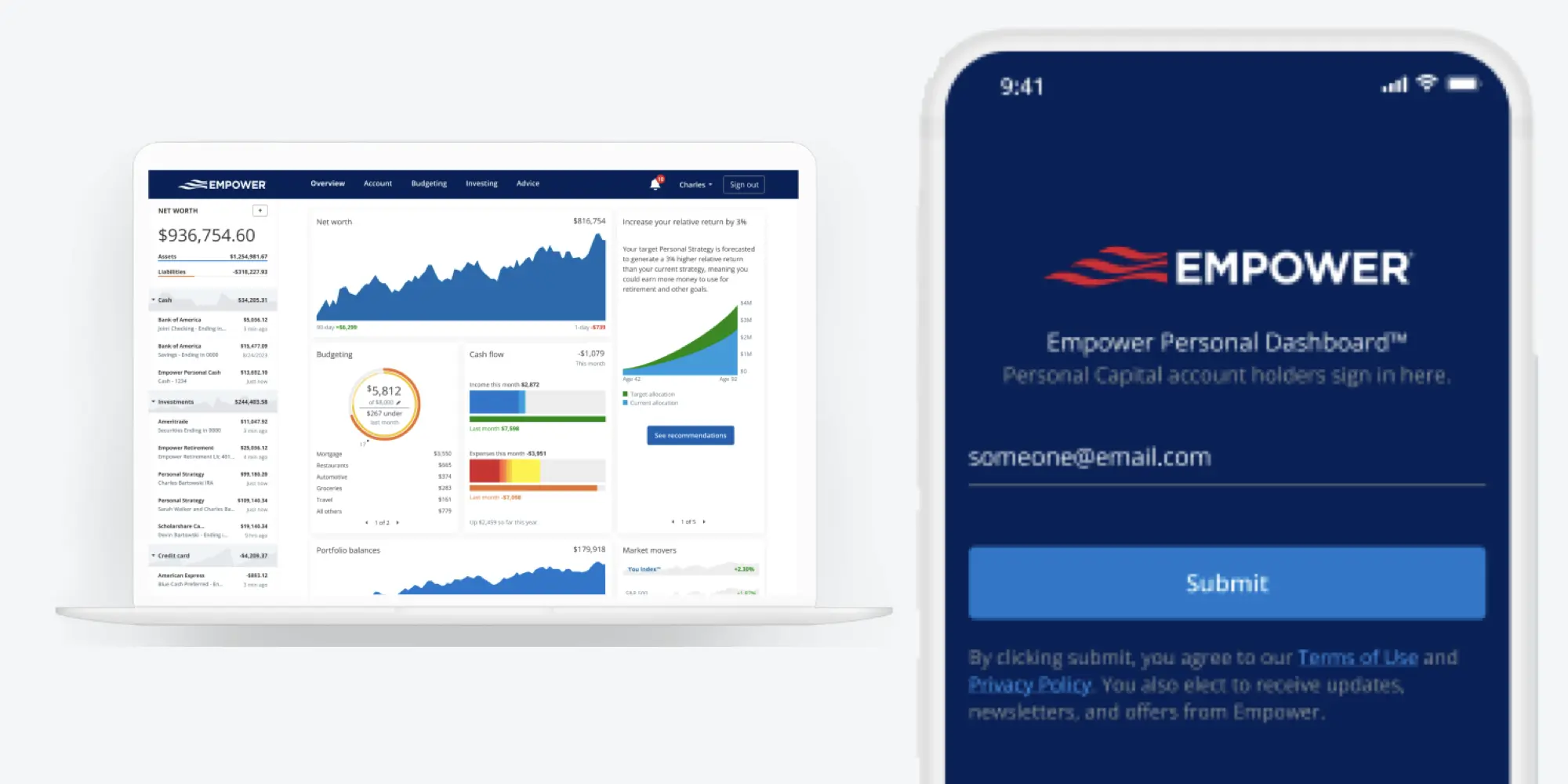

Empower Personal Dashboard Review

A few years ago, my wife and I opened a new chapter in our financial journey as we resolved to make 2019 the year we learned more about investing. Whether I was reading books on the subject or exploring other blogs for advice, there was one recommendation I came across again and again: Personal Capital — which is now part of Empower and is known as the Empower Personal Dashboard....

Money Management Product Reviews

Mana App Review: The Neobanking App for Gamers

One of the most intriguing trends I've seen emerge since I've been following FinTech is the advent of niche neobanks. These days, you can find apps geared towards certain communities, interests, and more. Among the latest examples I've seen of this is an app called Mana, which bills itself as the best debit card for gamers. Now, I may not be a big gamer, but I do know a thing...

Money Management Product Reviews

Ibotta App Review (2024)

I remember the first time I was introduced to the concept of digital coupons. For some reason, I was looking at the website for my local grocery store when I found a section dedicated to coupons. At the time I was confused about how you redeemed these coupons since they weren't in the typical print-and-clip format but, soon enough, I realized that I just needed to link them to my...

Money Management Product Reviews

The Good and Bad of Credit Karma in 2024

So Credit Karma might not be able to tell you exactly what your credit score is but the truth is you have so many scores that it hardly matters. What makes this free service great isn’t necessarily the credit scores it offers you but the tools it gives you to protect, monitor, and improve your overall credit.

Money Management Product Reviews