Category: Small Business News

Small Business News

Small Business News

SBA and Score Announce Small Business Week Virtual Summit

With National Small Business Week quickly approaching, the U.S. Small Business Administration (SBA) and SCORE have announced a virtual summit event. About the event: On April 30th and May 1st, the SBA and SCORE will co-host the 2024 National Small Business Week Virtual Summit. The special event will feature educational webinars with actionable insights, business resources, networking opportunities, a virtual exhibitor hall, and more. Additionally, as part of the programming,...

Small Business News

Amex Increases Grants for 4th Historic Small Restaurant Program

American Express has launched its latest Backing Historic Small Restaurants Program — and has significantly increased the grant money up for grabs. About this year's Backing Historic Small Restaurants Program: For the fourth annual Backing Historic Small Restaurants Program, American Express and the National Trust for Historic Preservation have announced that it will not only double the number of grant recipients but also increase the total funding. This year, 50 historic...

Small Business News

Barclays Unveils Fourth Annual "Small Business Big Wins" Contest

Barclays has announced that its "Small Business Big Wins" contest will be returning for its fourth year. About the contest: Entries for the fourth annual Small Business Big Wins program are now open. Once again this year, the content will offer up a total of $255,000. This includes one $60,000 Grand Prize winner as well as a $40,000 Second Place Prize winner and a $20,000 Third Place Prize winner. Seven...

Small Business News

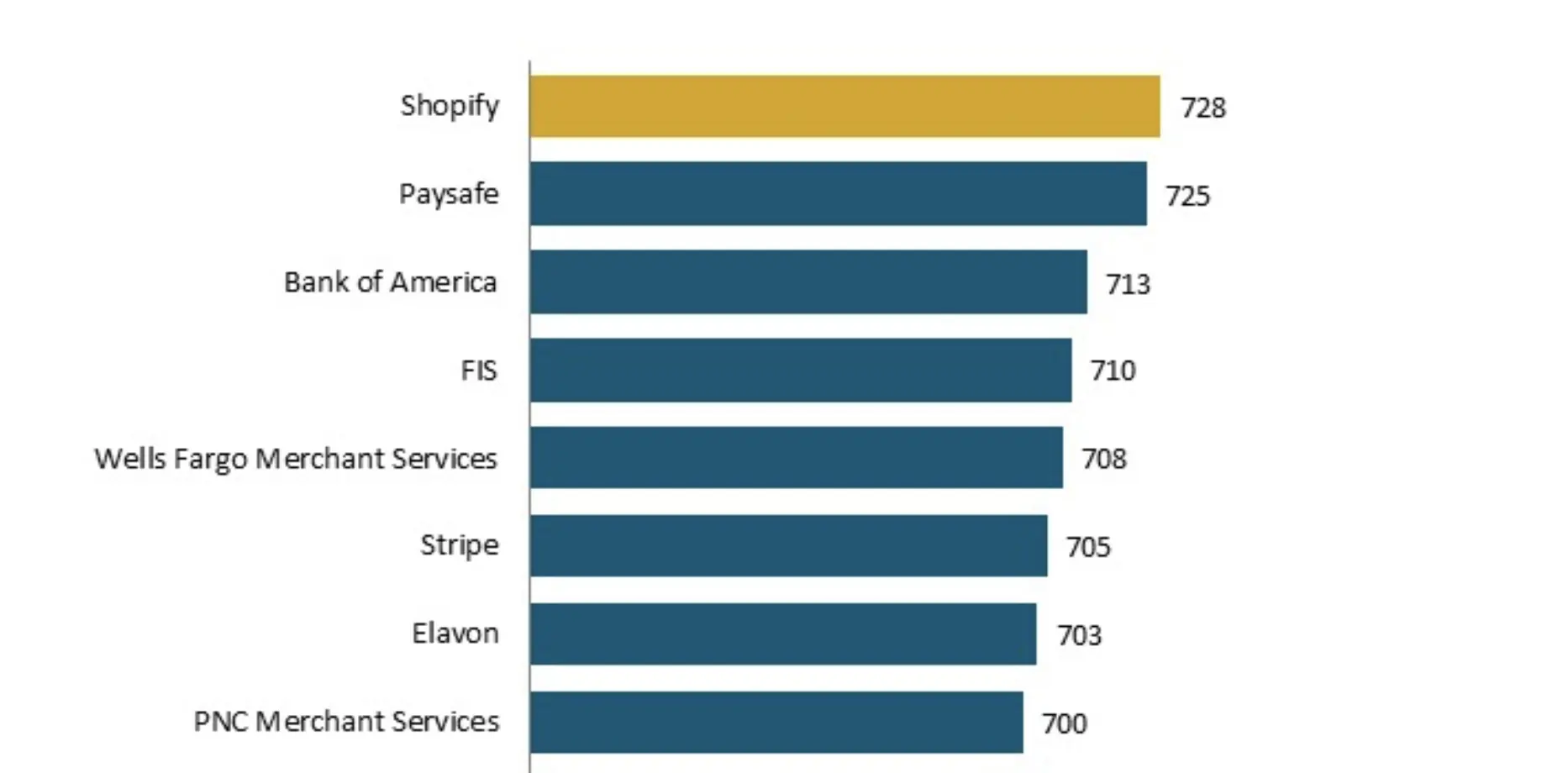

Survey: 94% of Small Business Merchants Accept Card Payments

A new survey highlights how the vast majority of small businesses are now accepting modern forms of payments — although satisfaction with some popular payment platforms is waning. About the survey results: J.D. Power has released its 2024 U.S. Merchant Services Satisfaction Study, which compiled responses from 5,383 small businesses. Conducted between September and November of last year, the survey inquired about provider satisfaction is several areas, including the cost...

Small Business News

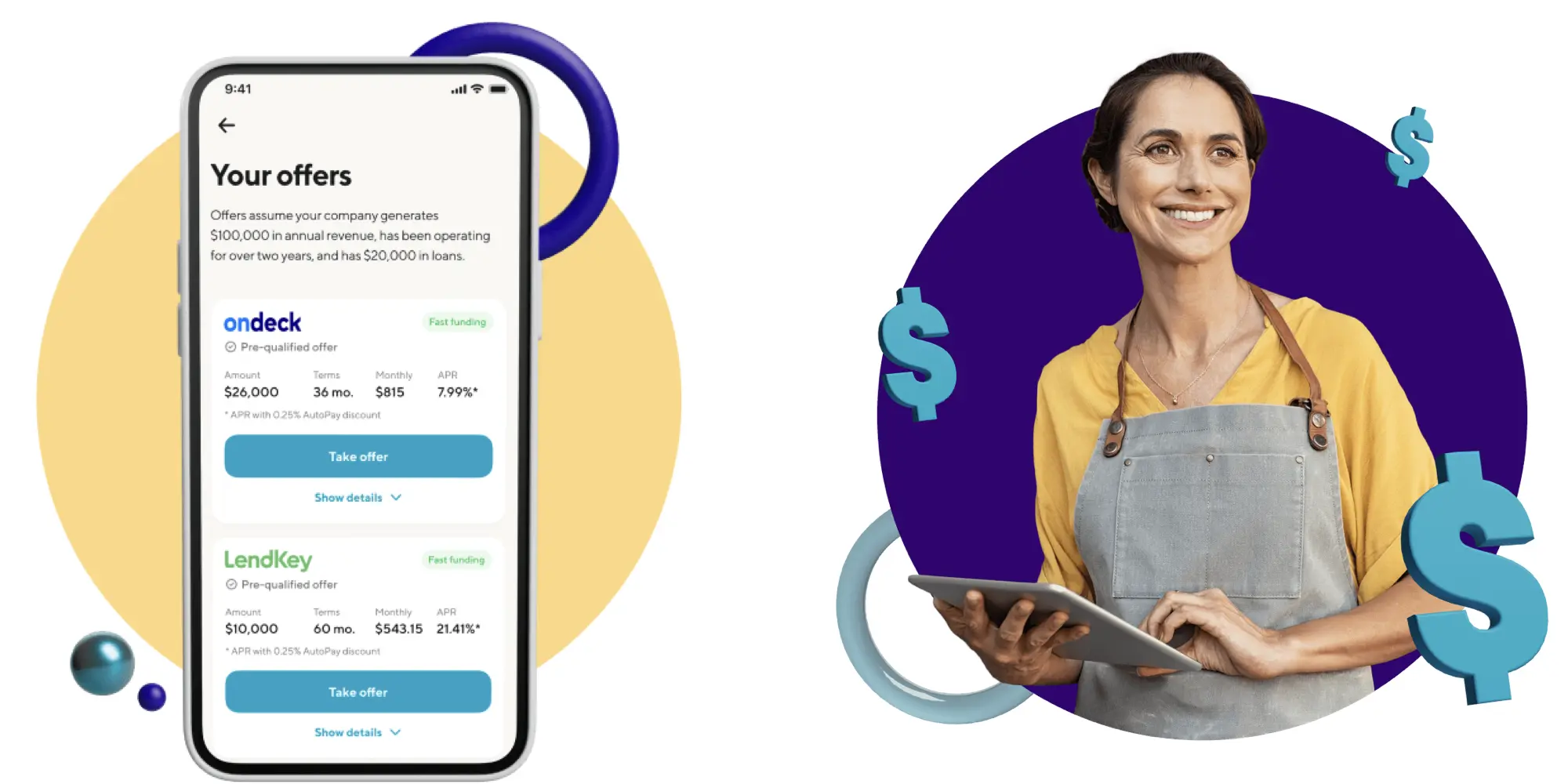

SoFi Launches Marketplace for Small Business Loans

SoFi is bringing a small business loan hub to its core user experience. About the marketplace: SoFi has announced an expansion of its small business marketplace. Now, small businesses can connect to the bank's network of providers and view funding options within the SoFi ecosystem. The loan marketplace can be found at SoFi.com/Small-Business-Loans. Among the loan types/users currently supported by SoFi's marketplace are expansion loans, equipment loans, working capital, payroll...

Small Business News

Survey: 23% Considering Starting a Small Business in 2024

Intuit has released its Entrepreneurship in 2024 Report, which features some interesting tidbits. About the findings: Intuit's report was derived from surveying more than 4,500 adults in the United States. Headlining the report is the fact that nearly one-quarter (23%) of respondents stated that they considered starting a business in the new year. Members of Gen Z were the most likely to be mulling the idea, with 28% responding affirmatively....

Small Business News